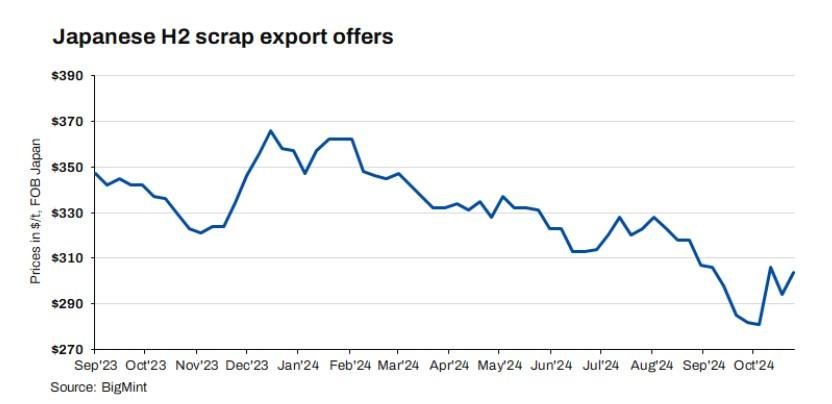

Japanese H2 scrap export offers climbed w-o-w, driven by recent deals concluded for Taiwan, where mills favoured competitively priced Japanese scrap over US bulk cargos. Additionally, domestic H2 collection prices in Japan rose, adding upward pressure on export offers. Limited deep-sea cargo interest from Vietnam and South Korea further restricted buyer options, lending additional support to higher Japanese export prices.

As a result, BigMint’s weekly assessment of Japan’s H2 scrap export offers increased by JPY 2,200/t ($14/t) to JPY 46,200/t ($304/t) FOB Tokyo Bay, up from JPY 44,000/t ($291/t) the prior week.

In the domestic market, H2 scrap prices increased for the second straight week, according to the Japan Iron and Steel Association. Average prices rose by JPY 300/t ($2/t) w-o-w to JPY 38,000/t ($250/t) on 23 Oct. Kanto saw a hike of JPY 100/t ($1/t) w-o-w to JPY 41,300/t ($272/t), and in Kansai, prices surged by JPY 800/t ($5/t) w-o-w to JPY 36,400/t ($240/t). Meanwhile, Chubu’s offers remained stable w-o-w at JPY 36,200/t ($238/t).

Other market updates

Vietnam: Vietnam’s imported scrap market remained subdued during the week, with weak domestic demand and low government investment disbursement hindering buying interest. Offers for Japanese H2 scrap ranged from $345-355/t CFR, but bids stayed lower at $330-340/t CFR, showing limited appetite for high-priced material. Mills largely monitored from the sidelines, expecting potential declines in spot H2 prices. In the deep-sea segment, US and Australian-origin HMS (80:20) offers were steady at $375/t and $370/t CFR Vietnam, respectively, but persistent bid-offer gaps led to limited activity as buyers found prices unappealing and held off on large-volume purchases.

Taiwan: Taiwan’s imported scrap market saw increased activity and prices, especially for Japanese-origin scrap. Two bulk H1/H2 50:50 Japanese-origin deals were concluded at $335-337/t CFR Taiwan, aligning with higher Japanese export prices. Meanwhile, US-origin containerized 80:20 scrap was less attractive to Taiwanese mills due to comparable pricing for Japanese bulk offers.

Locally, Feng Hsin Steel raised rebar and domestic scrap prices by TWD 200/t, marking the third consecutive weekly hike to manage rising global scrap costs. Additionally, with Taiwan’s peak steel consumption season underway, supported by favourable weather and increased construction activity, local demand and prices are expected to remain buoyant.

South Korea: South Korea’s imported scrap market remained sluggish through the week, as domestic prices for H2-equivalent light A-grade scrap fell to around KRW 380,000/t ($275/t), down from KRW 390,000-410,000/t. Heavy A-grade scrap also slipped, pressured by slow demand for downstream steel products and the upcoming winter season, which traditionally weakens construction activity.

Domestic scrap prices stayed competitive due to currency exchange rates, with import demand restrained by low steelmaker profitability. Mill bids for imported HS, shredded, and Shindachi Bara scrap grades held at levels between JPY 49,000-51,000/t ($322-335/t) CFR Korea as mills avoided high-cost imports, contributing to limited transaction activity.

Article Credit: Bigmint